SELECT LOCATION

- Indonesia

- Bali

-

Gapura Bali

Gapura Bali - Visit by region

-

- Jakarta

- Bali

- Japan

- Myanmar

-

Myanmar Real Estate Conversation

Myanmar Real Estate Conversation - Visit by region

-

Hong Kong Commercial Real Estate Market: Gradual Rebound of Leasing and Investment on Market-Expected Easing Rates - CBRE launches Hong Kong Real Estate Market Outlook 2024

Hong Kong commercial real estate market showed mixed trends across sectors in 2023. The year saw a noticeable decline in investment volume, while office and retail leasing showed improved velocity. The market faces challenges for a strong recovery in 2024 as geopolitical and economic uncertainties remain in place, however, Hong Kong’s business environment is expected to improve, according to CBRE Hong Kong’s 2024 Market Outlook.

“The commercial real estate market has experienced a slower-than-expected recovery in 2023. Negative carry deepened, and investment appetite halved, hitting a 15-year low as financing costs reached a 22-year high. Hong Kong’s economy will continue to recover in 2024 as the Chinese economy strengthens while potential interest rate cut will improve investment market momentum. Overall property demand is expected to see moderate growth in 2024,” said Marcos Chan, Executive Director, Head of Research, CBRE Hong Kong.

Review and Commentaries

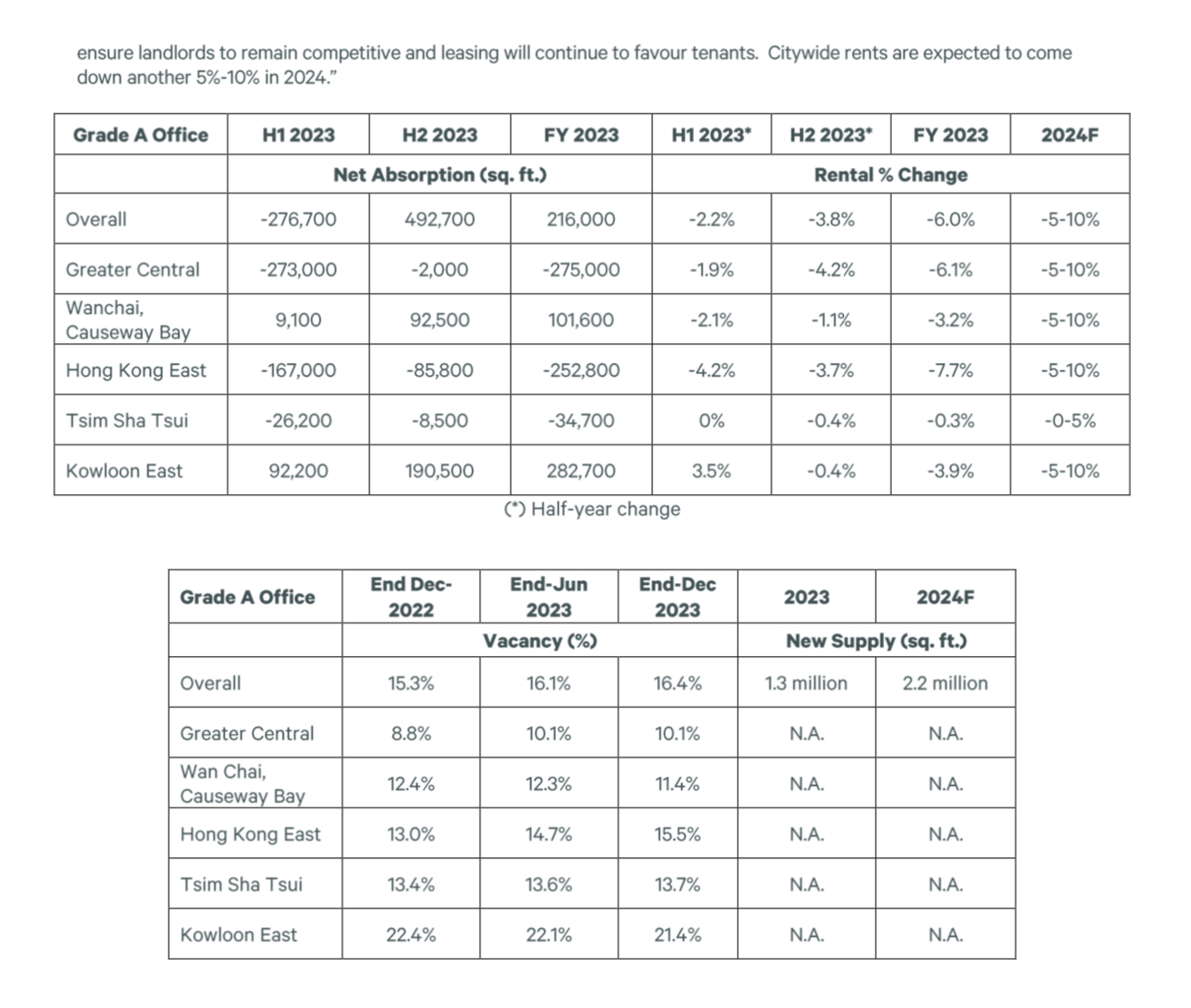

Grade A Office

Ada Fung, Executive Director, Head of Advisory & Transaction Services – Office Services, CBRE Hong Kong: “The office market posted moderate growth in new leasing volume with vacancy rising to another all-time high. Although there were some upgrading activities in Kowloon, cost saving was still the main theme for the year. Fully-fitted office space was sought after as relocating tenants sought to minimize CapEx. For 2024, we expect Hong Kong’s financial markets to recover and support a mild growth in office demand. Companies, however, will remain largely cost-sensitive. High vacancy will ensure landlords to remain competitive and leasing will continue to favour tenants. Citywide rents are expected to come down another 5%-10% in 2024.”

(*) Half-year change

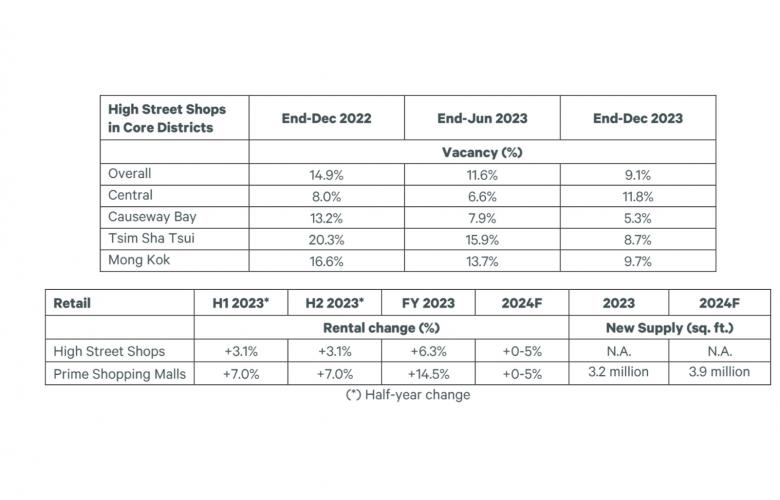

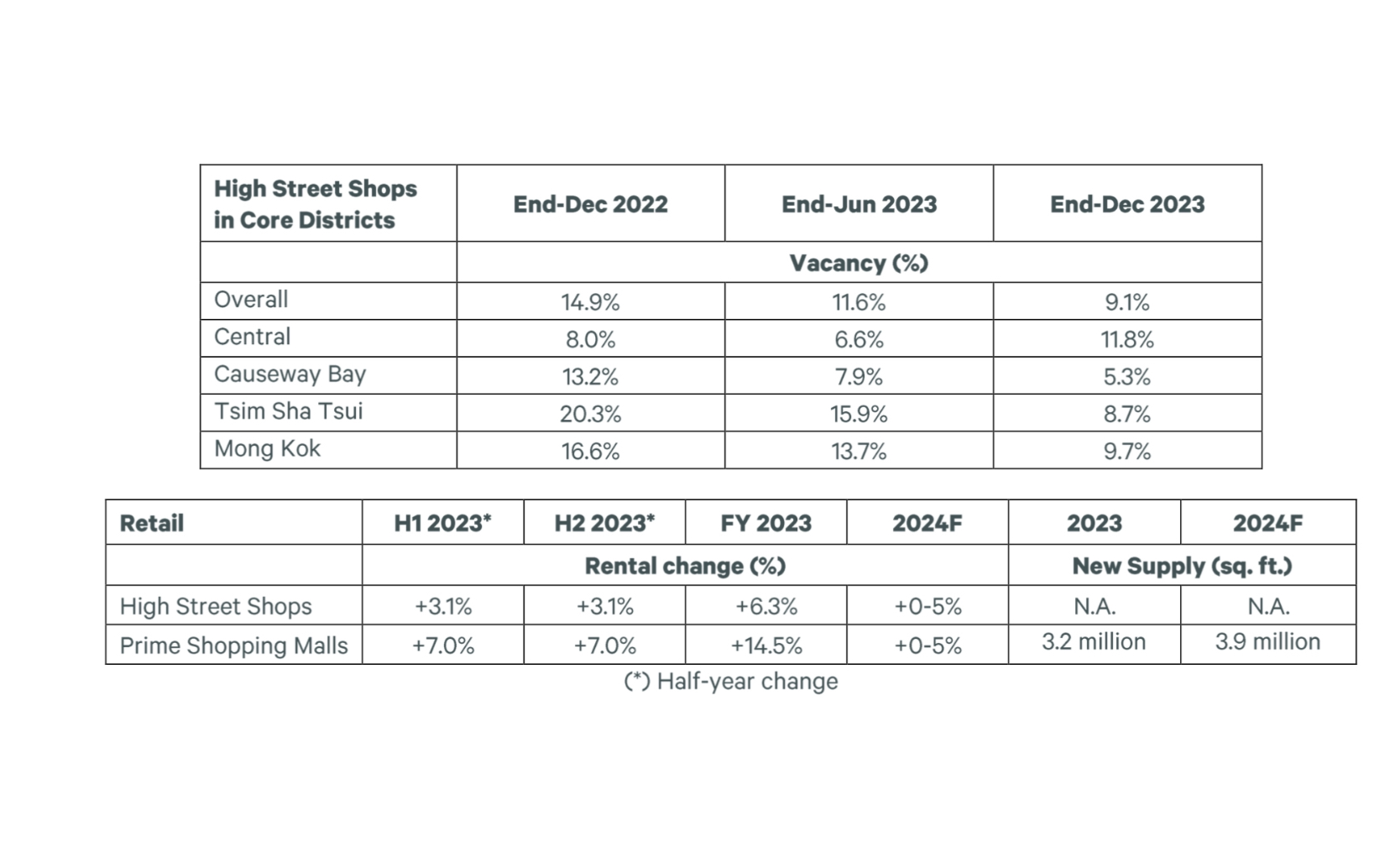

Retail

Lawrence Wan, Senior Director, Head of Advisory & Transaction Services – Retail, CBRE Hong Kong: “The retail leasing market has improved significantly over the year, and even broke a record in new leasing volume of high-street shops. Looking ahead into 2024, recovery of the Chinese economy, anticipated strengthening of the RMB and potential interest rate cuts will lend support to tourist and local consumptions. Attractive rental levels will also encourage retailers to reconfigure their branch networks. Retail leasing is expected to stay healthy. A moderate rental growth in the range of 5% is possible for high street shops in 2024.”

(*) Half-year change

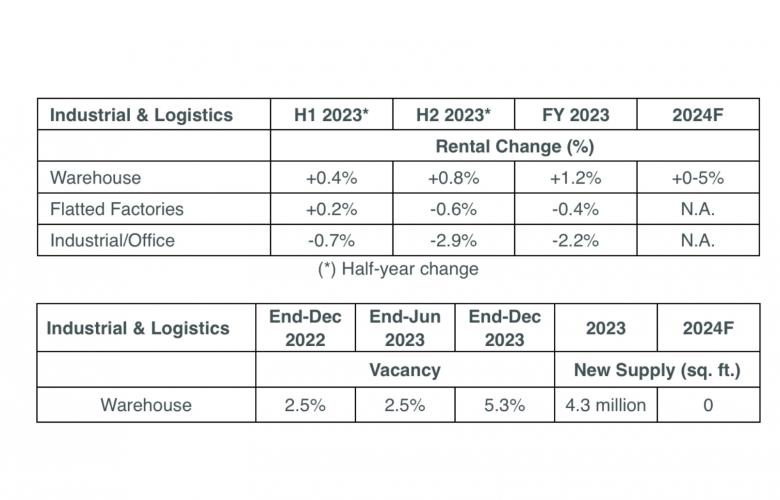

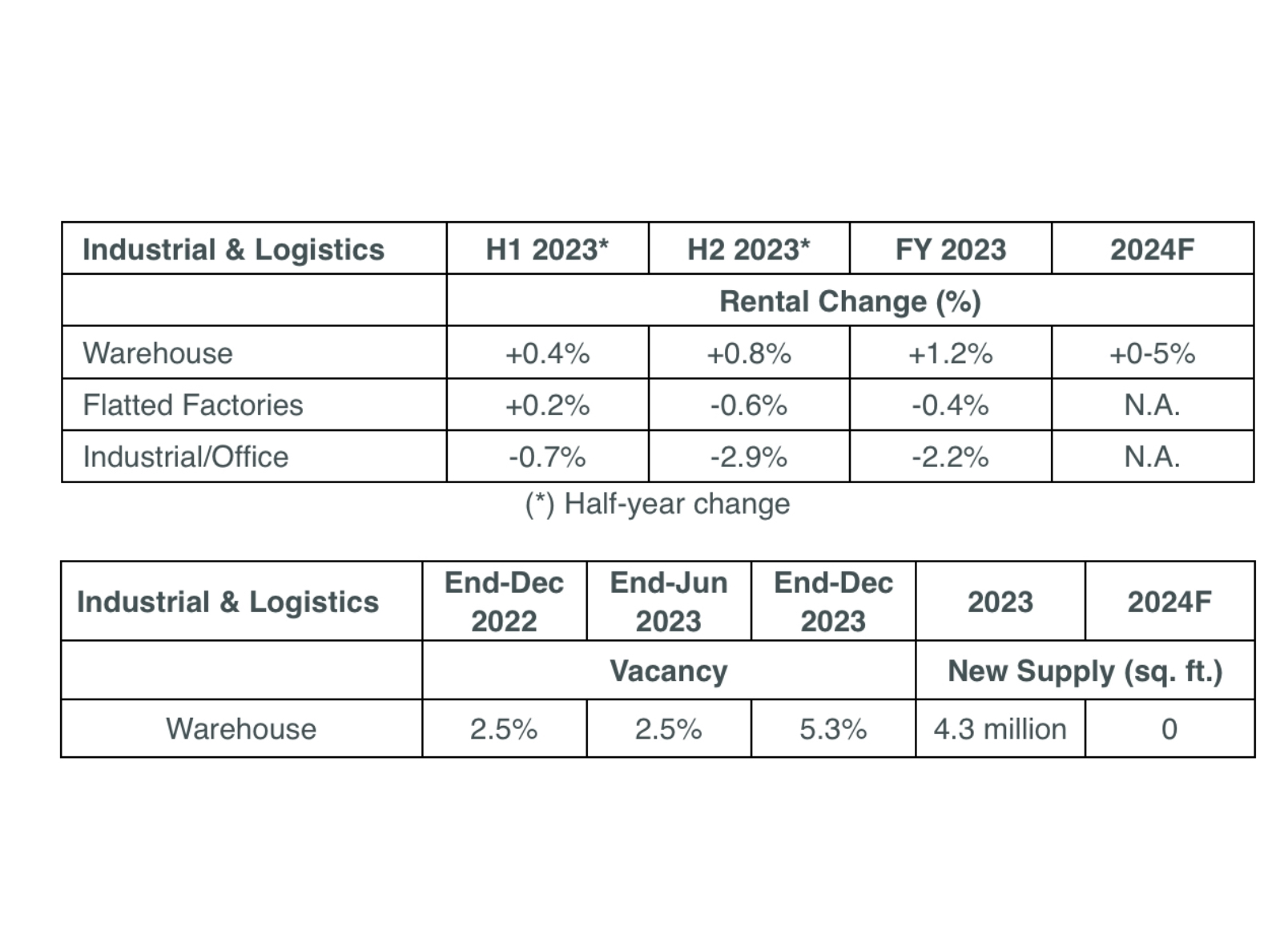

Industrial

Samuel Lai, Executive Director, Head of Advisory & Transaction Services – Industrial & Logistics, CBRE Hong Kong: “Weak trade flow ensured a subdued leasing environment for industrial properties in 2023. Traditional occupier groups such as 3PLs were slow in leasing, but emerging trades brought some new demand for space. The outlook for 2024 would depend on the pace of recovery of global trade flow. Further strengthening of the Chinese economy will gradually improve Hong Kong’s exports and hence potential demand for logistics space. The return of some expiring space in H1 2024, however, will require landlords to remain flexible. Warehouse rents are expected to edge down within a 5% range in 2024.”

(*) Half-year change

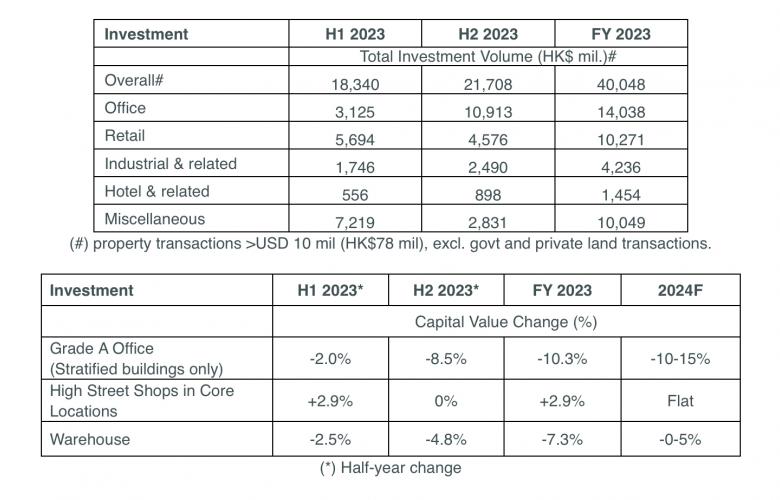

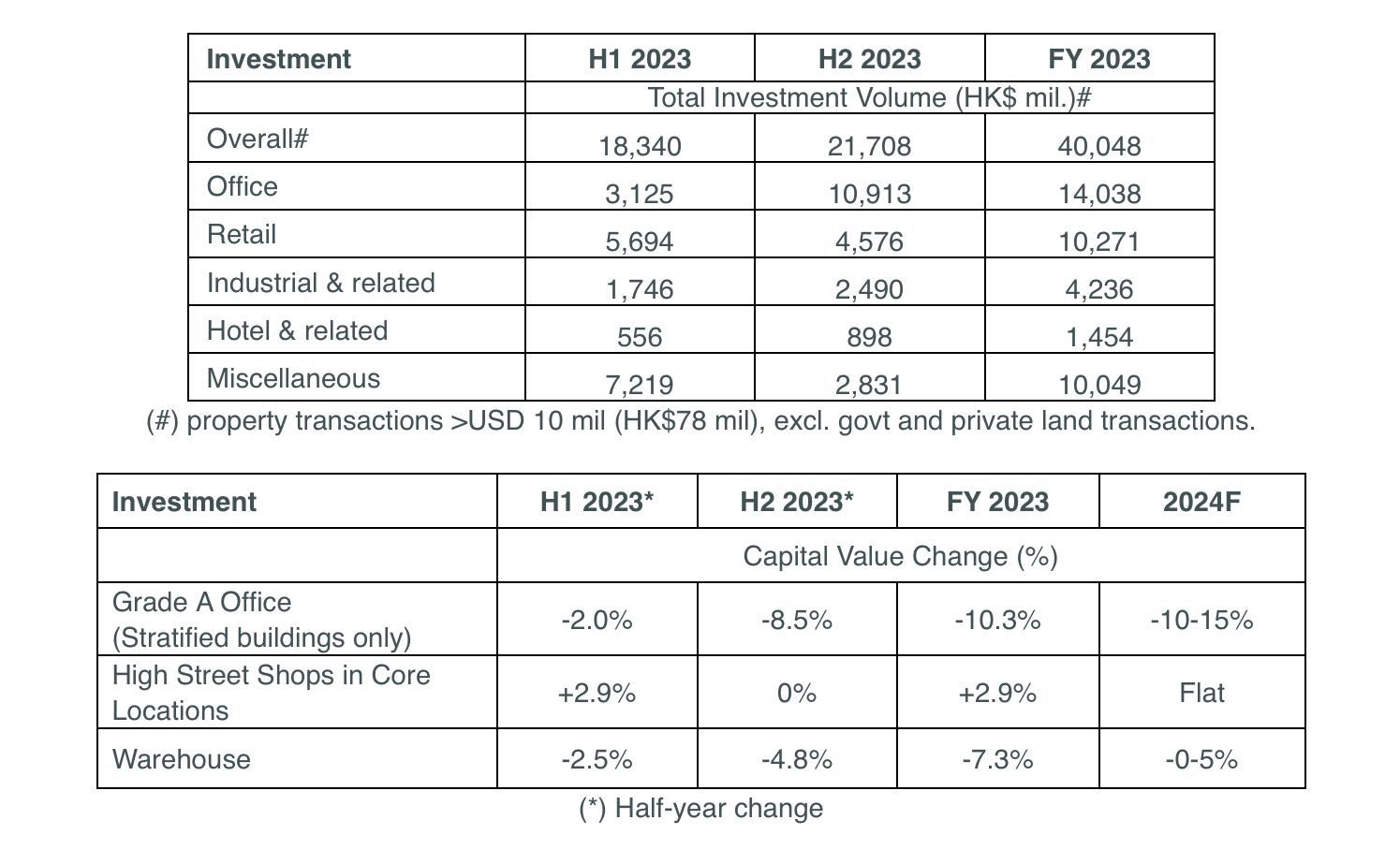

Capital Markets

Jonathan Chau, Executive Director, Head of Investment Property & Private Office, Capital Markets, CBRE Hong Kong: “Deep negative carry, banks’ cautious lending, economic and geopolitical uncertainties as well as weak demand in some local property sectors combined to half investment volume year-on-year in 2023. It has also hit a 15-year low. Looking ahead, anticipated rate cuts will likely improve business and investment market sentiment and result in a recovery in deal flow in 2024. Relatively high levels of financing costs, however, will prevent a v-shape rebound in transaction volume and capital values.”

(#) property transactions >USD 10 mil (HK$78 mil), excl. govt and private land transactions.

(*) Half-year change