SELECT LOCATION

- Indonesia

- Bali

-

Gapura Bali

Gapura Bali - Visit by region

-

- Jakarta

- Bali

- Japan

- Myanmar

-

Myanmar Real Estate Conversation

Myanmar Real Estate Conversation - Visit by region

-

Colliers International have released their Colliers Singapore Office Quarterly Q1 2019 Report

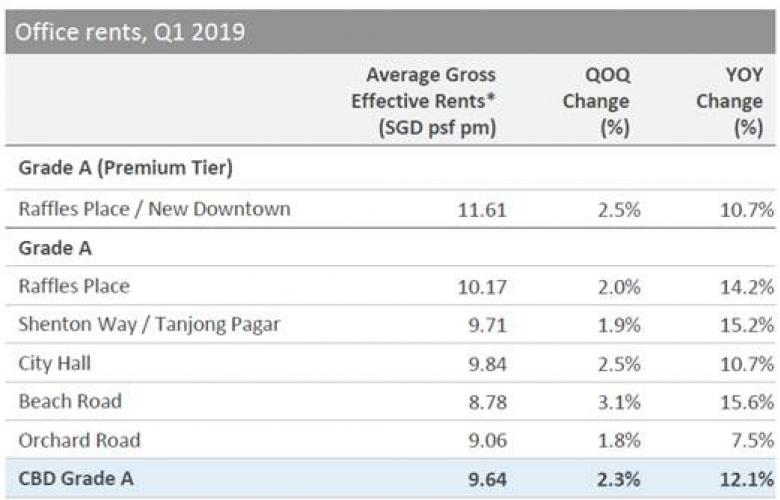

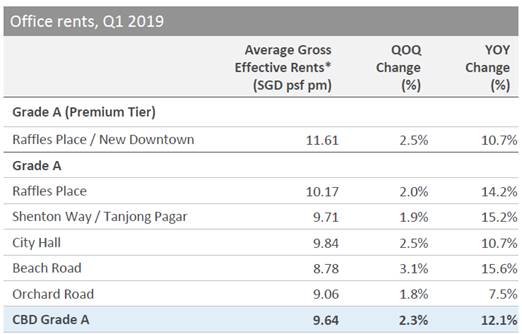

Premium & Grade A office rents in Singapore’s central business district (CBD) continued their growth momentum, posting a broad-based increase in Q1 2019. According to Colliers Research’s latest market report, average prime CBD office rent rose for the seventh straight quarter in Q1 2019 to SGD9.64 per square foot per month (psf pm) – up by 2.3% from the previous quarter and 12.1% year-on-year (YOY).

At a glance:

The firmer rents were driven by tighter vacancy across most micro-markets with higher demand mostly from technology and flexible workspace operators. Increasing landlord confidence also underpinned lower incentives and rental uplift in the CBD.

In addition, the continued recovery in the office property market also reflects the growth in the services sector, which expanded by 4.8% on a quarter-on-quarter (QOQ) seasonally-adjusted basis in Q1 2019, according to the latest GDP figures from the Trade and Industry Ministry earlier this month.

Ms. Tricia Song (宋明蔚), Head of Research for Singapore, Colliers International, said, “Following the strong growth in office rents (up by 15% YOY) in 2018, we expect CBD Grade A rents to remain firm in 2019, growing by 8% for the full-year amid supply shortfall and healthy occupier demand. Beyond that, we estimate that prime CBD office rents could experience a slight decline in 2021 in anticipation of higher supply in 2022, before a rebound thereafter.”

New proposed schemes to rejuvenate the CBD under the Draft Master Plan 2019, if taken up, could further crimp the availability of office space in the city and drive up rents in the medium-term. Colliers recommends that affected occupiers should explore options to move to newer space within the CBD, or relocate to city fringe offices or even to business parks, if applicable. Investors could also look to add value with redevelopment premiums to older buildings.

Source: Colliers International

Beach Road micro-market led the way in Q1 2019

Rents at City Hall and Beach Road micro-markets grew faster than average, as landlord confidence was boosted by the upcoming rejuvenation in the precinct – the new Guoco Midtown and the redevelopment of Shaw Tower are due to complete in 2022 and 2023, respectively. In particular, the Beach Road micro-market led rent growth in Q1 2019, rising by 3.1% QOQ and 15.6% YOY to SGD 8.78 psf pm.

Leasing and vacancies

In Q1 2019, technology companies Zendesk and Grab expanded, with a takeup of 50,000 sq feet (4,645 sq metres) and 32,000 sq feet (2,973 sq m) in Marina One West Tower respectively. Meanwhile, flexible workspace operator Regus occupied three office floors and one retail floor (over 30,000 sq feet or 2,787 sq m) in the newly completed 18 Robinson.

CBD Grade A vacancy tightened significantly, to 3.9% from 5.4% as at the end of Q1 2019. However, the move by UBS to 9 Penang Road, and potential surrendering of space by other financial occupiers, should provide some relief to occupiers in the core CBD in the next few quarters.

Ms. Song added, “We project total net demand of 857,000 sq ft from occupiers for prime office space in the CBD in 2019 and this should outstrip supply, potentially putting upward pressure on rents. In particular, we expect CBD Grade A net absorption should be driven mainly by technology and flexible workspace sectors’ expansionary demand.”

Deals remain robust in a rising rental market

In Q1 2019, the average imputed capital value of CBD Grade A office properties rose 1.2% QOQ and 7.6% YOY to SGD2,453 psf. This reflected SGD953 million worth of transactions seen in the quarter, pushing the rolling 12-month volumes of office and mixed-use commercial transactions to SGD5.39 billion, an 18% QOQ increase. Meanwhile, CBD Grade A implied yields remained flat, ranging between 3.2% and 3.7% on average.

Source: Colliers International

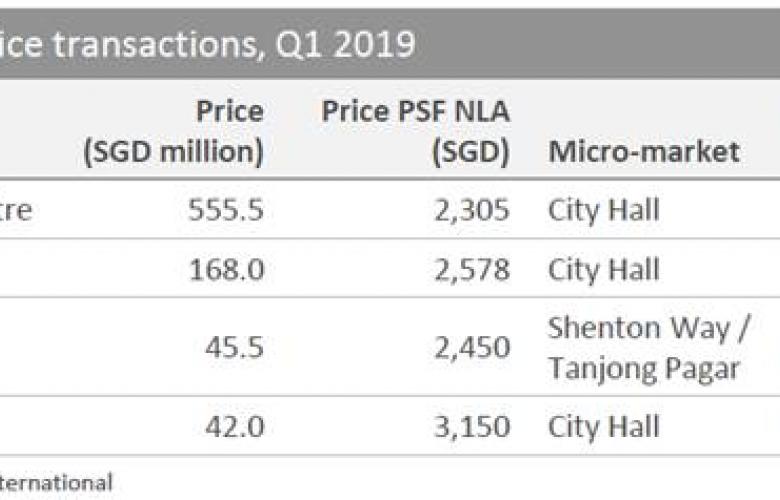

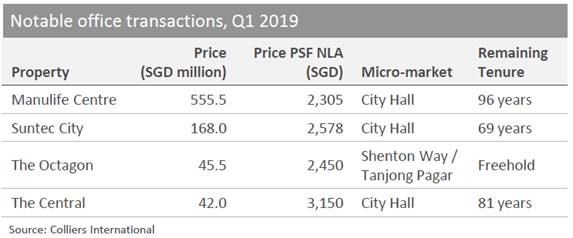

Notable office investment transactions in the quarter included: Manulife Centre which was jointly acquired by ARA Asset Management and British property group Chelsfield for SGD555.5 million; six levels at Suntec City which were reportedly sold to Alpha Investment Partners for SGD160 million and another floor at the same property that was sold to an unnamed party for SGD8 million; three levels at The Octagon which were reportedly acquired by a Singapore-incorporated company linked to Indonesian conglomerate Central Cipta Murdaya for SGD45.5 million; and the sale of office units at The Central for SGD42 million to Chuan Hup Holdings..

Mr. Jerome Wright, Director, Capital Markets & Investment Services, Colliers International, said, “We expect capital values to trail the projected rent growth and hence yields to remain largely stable over 2019-2021, mainly due to the hefty weight of global capital directed towards gateway cities. Moreover, the Singapore office market offers favorable fundamentals with the expected supply shortfall over 2019-2021.”

For more information about the Singapore Office market email Ms. Tricia Song (宋明蔚), Head of Research for Singapore or Mr. Jerome Wright, Director, Capital Markets & Investment Services, Colliers International via the contact details below.

Similar to this: