SELECT LOCATION

- Indonesia

- Bali

-

Gapura Bali

Gapura Bali - Visit by region

-

- Jakarta

- Bali

- Japan

- Myanmar

-

Myanmar Real Estate Conversation

Myanmar Real Estate Conversation - Visit by region

-

Tom Moffat from CBRE explains that big ticket deals and diverse geographic mix are favoured by investors when deploying capital into global real estate.

International real estate continues to serve as an attractive asset class for investors, with Asian outbound investment into the sector posting significant year-on-year gains in the first half of 2017. This was led largely by the preference of investors for big ticket deals in the global real estate sector.

Asian outbound investors are rebalancing real estate portfolios internationally. “The appetite of Asian investors for high quality cross-border real estate assets remains solid and sustainable for the foreseeable future,” said Tom Moffat, Executive Director, Capital Markets, CBRE Asia. “However, the type of transactions and the geographic and sectoral diversity is where we see the most significant change in 2017.”

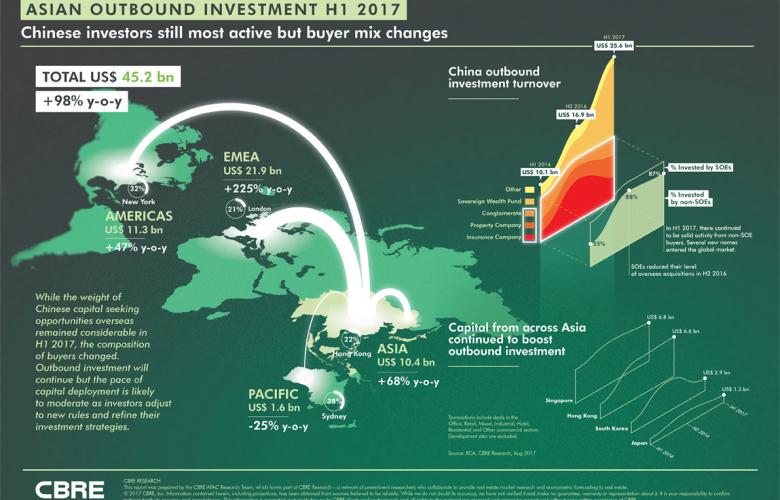

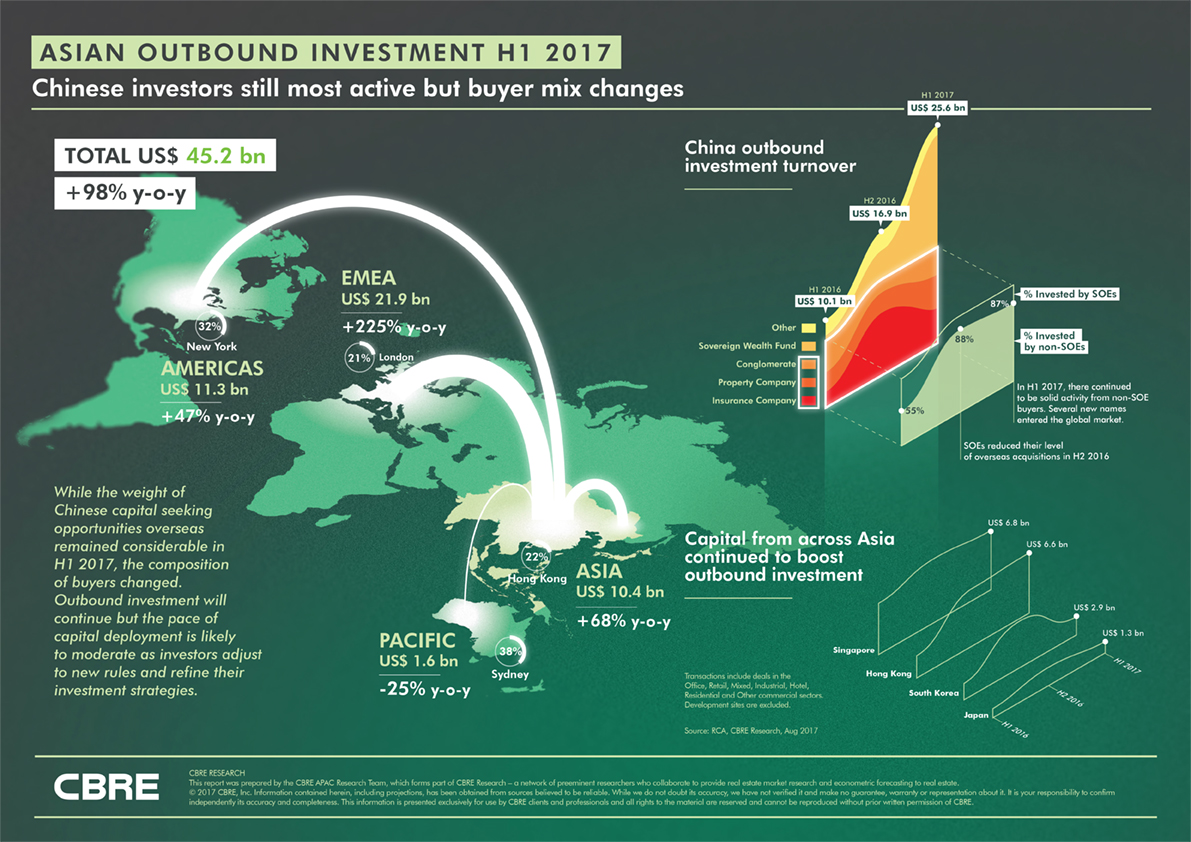

Asian investment H1 2017 at a glance (according to CBRE):

Where Asian funds were invested (first half of 2017):

Asian outbound investment H1 2017. Picture credit: CBRE

Asian outbound investors additional key findings:

Non-China investors more active: Singapore (US$6.8 billion), Hong Kong (US$6.6 billion) and South Korea (US$2.9 billion) remain active outbound investors and continue to deploy capital as Chinese investors rebalance portfolios.

Number of portfolio deals rising: They are now more likely to deploy capital via portfolio transactions. In the first half of 2017, 26 portfolio deals were committed versus 13 in the first half of 2016.

Destinations becoming more diverse: They now look beyond gateway cities when deploying capital into real estate. In the first half of 2017, the top five urban destinations comprised of 31% of all total Asian outbound capital compared to 54% in the first half of 2016.

China outbound diversity: Chinese capital continues to be deployed differently relative to the region. In the first half of 2017, the primary destinations of outbound investment were office (Americas), logistics (EMEA) residential (Japan) and hotels (Australia), representing the pull of diverse and quality real estate assets globally.

Source: CBRE

Similar to this:

JLL names Shanghai, Beijing, Guangzhou and Bangkok as Rising Giants of growth cities.